This article was published on FactSet’s Insights blog.

It is easy to imagine the predicted impacts of climate change are relevant mostly in the distant future. But when making investment decisions, giving short shrift to short-term climate scenarios could result in missed opportunities. Let’s take a look at why it’s important to consider both short- and long-term circumstances.

So much of the conversation around climate impact focuses on ambitious goals set for distant decades; it’s why you’ll see many net zero initiatives for 2050 or even 2100. Of course, a lot of unpredictable things will happen between now and then.

Asset managers who focus on far-off dates could sometimes be prone to bias risk mitigation. There is a sense that all climate goals must first be accomplished through decarbonization—an assumption that amounts to an eventual 100% divestment from fossil fuels paired with an equally ambitious investment in renewables. Current adaptation is relegated to an assumption that short-term scenarios don’t require immediate action.

Yet as we’re reminded regularly by the latest weather events, gradual shifts in climate can have compounding effects that become significantly more pronounced long term. The cumulative impact of the changes is accelerated. For example, the way warming temperatures can trigger permafrost thaws that release more greenhouse gasses and hasten warming.

From an investment perspective, we believe it’s most important to accurately gauge the full variance of climate predictions. One way to try to achieve better investment returns is to get a better sense of the possibility of major disruptions and hedge against them.

Improvements in the design of climate scenarios and integrated assessment models go a long way toward increasing those probabilities. So too does the ability to run scenarios and models year after year, creating a short-run vision that translates to financial materiality for investors. By adding up multiple short runs, you get a better sense of what may happen in the long run.

Part of our confidence in creating multivariate scenarios encompassing “most-likely outcomes” comes from improvements in models that measure two types of risk long thought to be distinct: physical and transition risks.

Climate transition risk refers to potential financial and economic impacts that could arise as the world adapts to a low-carbon future—including impacts on businesses and markets as all players adjust their operations, technologies, and investments to align with climate policies and regulations.

Physical risk refers to the potential impacts of climate change and its related effects: extreme weather events such as temperature spikes and sharp changes in precipitation patterns. There is also potential for a significant rise in sea levels, which could affect infrastructure, communities, economies, and the environment itself.

Extreme weather events and related damage have accelerated in frequency and intensity, shifting physical risk increasingly into the present. At the same time, the cost of mitigation has fallen far more rapidly than anticipated, moderating the financial impact of the physical risk of the climate transition. The use of unified measurements for both types of risk increases the odds that short-term scenarios can be a vital tool for asset managers.

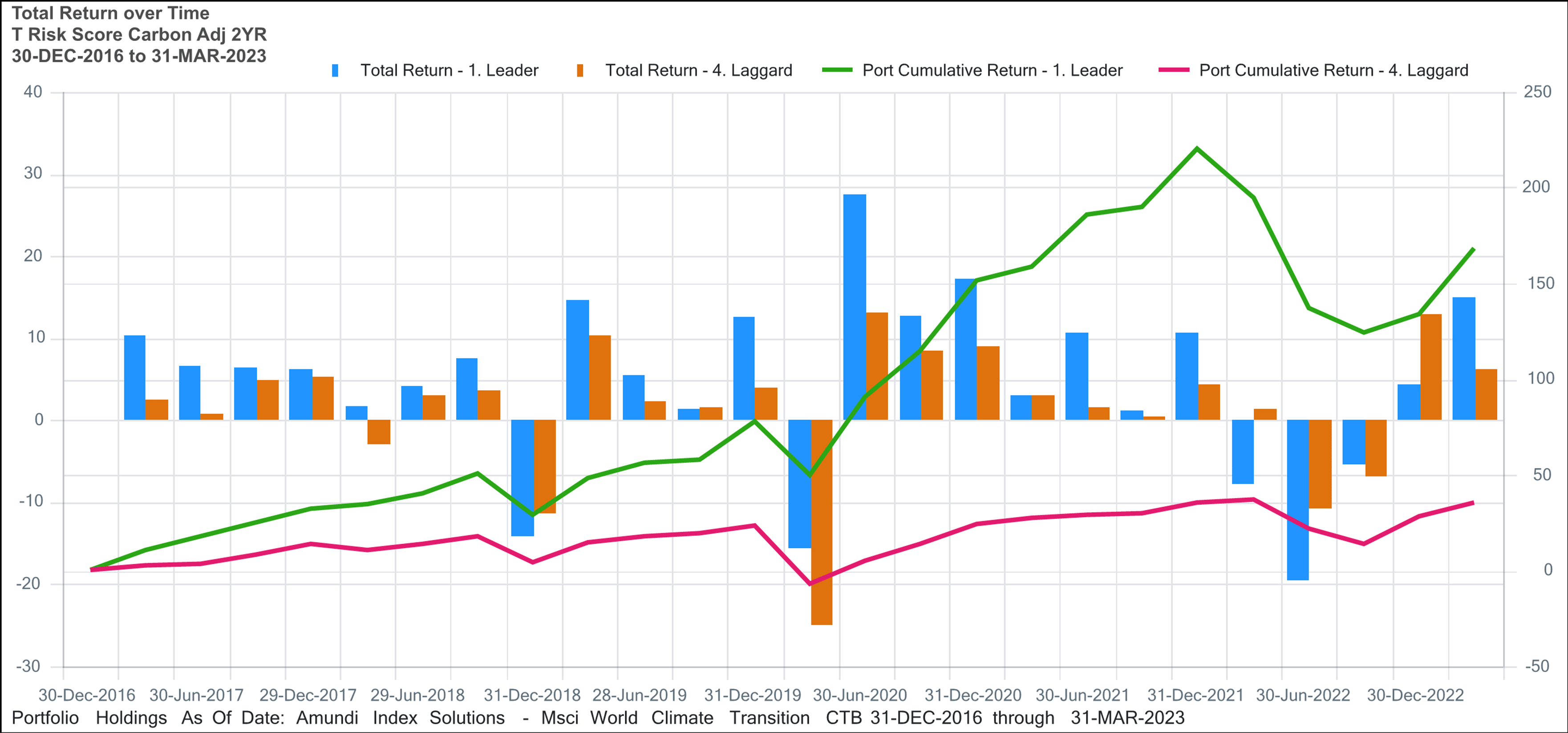

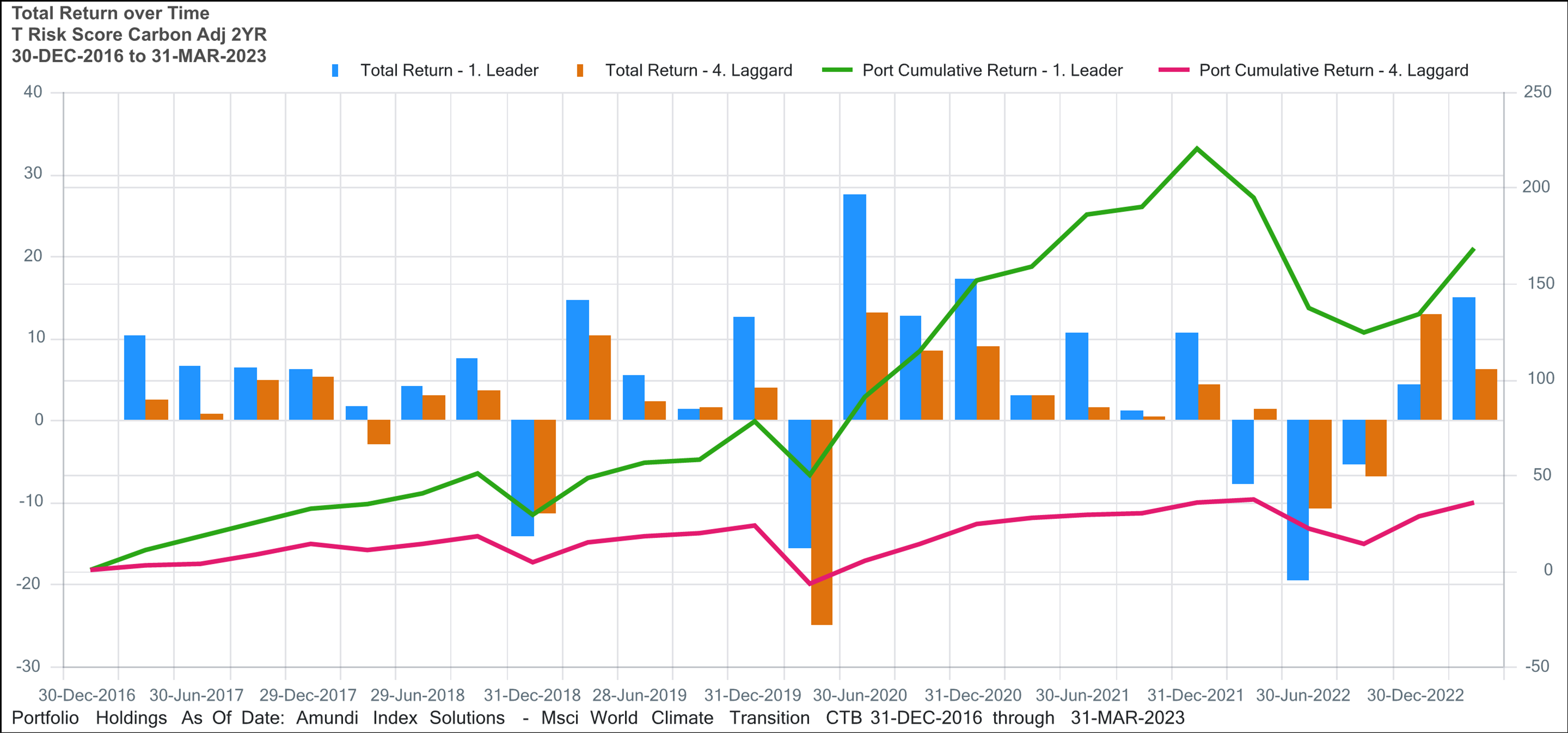

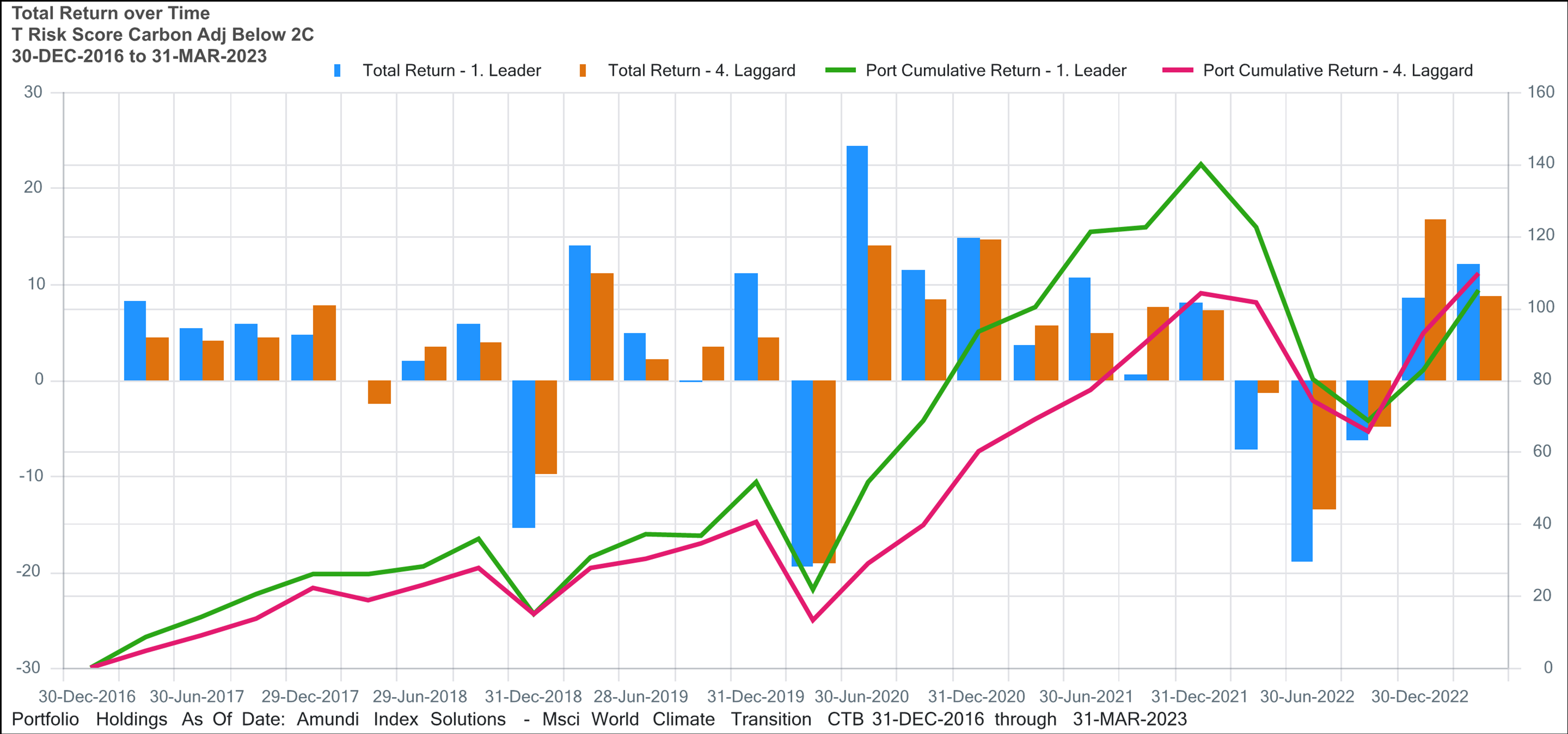

By subjecting the MSCI World Climate Transition Portfolio to a screening process, as shown in the two charts above, we identified companies that exhibit a heightened proficiency in adapting to immediate climate and carbon price shifts. This strategic approach focuses on a two-year transition risk effect, highlighting companies that demonstrate responsiveness to present-day climate dynamics and carbon pricing alterations, as opposed to the broader 10-year forecast adjustments.

How is this approach valuable?

- Immediate adaptability. By screening for companies that excel in coping with a two-year transition risk effect, we prioritize those that are quick to respond to the current climate and carbon price adjustments. This ensures that our portfolio includes companies that are not only well-prepared for present challenges but also positioned to capitalize on short-term opportunities resulting from these shifts.

- Holistic preparedness. Simultaneously considering both the two- and five-year time horizons is essential because it provides a more comprehensive view of a company’s transition readiness. While immediate adaptability is crucial, looking ahead to a five-year horizon allows users to gauge the sustainability of various strategies. This ensures that the companies that are selected don’t just react to short-term changes, but also have well-developed long-term plans for transitioning toward a low-carbon economy.

Incorporating transition risk assessment in both time frames allows users to strike a balance between short-term benefits and a sustainable future trajectory.

Yet climate change has shown that expectations for the future (both short term and long term) must account for variance. Climate projections are neither simplistic nor linear. They are not orderly. In fact, they contain multiple nonlinearities, multiple feedback loops, and multiple tipping points that can lead to abrupt shifts in energy and technology patterns.

That paradigm also applies to the climate’s impact on investments. An assumption of linear relationships between these factors will likely result in constant surprise, and underperformance.