By Pooja Khosla, Ph.D., Entelligent Chief Innovation Officer; Fenton Aylmer, President, Donadea, Inc. and Piyush Srivastava Market and Strategy Partner, Entelligent; and Partner and Head, BFSI Industry Advisory Group, North America, TCS. (This article is also available on TCS’ website.)

HIGHLIGHTS

- Many financial institutions have made net-zero commitments to align with the objectives of the Paris Agreement. However, this is no easy task.

- The calculation of climate transition risk necessitates scenario analysis, stress tests, and the adoption of a data analytics model.

- There are two approaches to calculating climate transition risk. Financial institutions must choose the best approach based on organization specific factors and requirements.

AN IRREVERSIBLE CHANGE

Climate risk is among the most significant macroeconomic forces impacting economic and business sustainability.

Over the past decade, direct damages from climate disasters have touched an estimated USD 1.3 trillion or around 0.2% of world GDP on average per year* —and financial institutions have not been immune. A central support of global economic and financial stability and growth, the banking industry is increasingly exposed to financial risks associated with the transition to a low-carbon economy.

Climate change risk manifests itself in many categories such as credit risk, market risk, operational risk, and reputational risk. Financial institutions and their regulators recognize that banks must manage these exposures to remain resilient and support the transition to a sustainable economy. A proactive and forward-looking approach to risk management—one that includes climate stress testing, scenario analysis, and risk disclosure—is essential.

Central banks and global regulators are taking incremental steps to ensure banks are prepared for these risks. We examine the role of data and analytics grounded in climate science in complying with global regulatory requirements and laws around climate risk disclosures.

TACKLING THE ISSUE

While financial institutions have embarked on several initiatives, meeting the goals of the Paris Agreement may still not be easy.

In 2019, the European Investment Bank, the European Union’s (EU) development bank, owned by EU member states, announced it would stop funding fossil fuel projects by the end of 2021. This decision adversely impacted some financial institutions exposed to fossil fuel-dependent assets. Meanwhile, the financial services industry is not a stranger to climate-related operational risk in action, bearing the physical impact of extreme weather events. Hurricane Sandy’s shuttering of Wall Street based banks and financial institutions in 2012 is a prominent example.

Despite focused efforts, the world’s largest banks are falling short in their efforts to manage climate risk and achieve the targets of the Paris Agreement. This conclusion was hammered home by a report released by the Institutional Investors Group on Climate Change (IIGCC), whose more than 350 members are mainly asset managers and owners. In its assessment of the low carbon initiatives of 27 banks in Asia, Europe, and North America, IIGCC found that the banking industry is still at a nascent stage of the transition. The report concludes that banks need to significantly ramp up decarbonization efforts to align with the goal of limiting global warming to 1.5°C (2.7° F) above pre-industrial levels.

THE REGULATORY LANDSCAPE

Regulators have mandated banks across the globe to disclose climate risk exposures.

They are having to run climate stress tests and disclose climate risk information to remain on track with the objectives of the Paris Agreement. Applicable regulations and industry standards include the Task Force on Climate-related Financial Disclosure (TCFD), the Network for Greening the Financial System (NGFS), the EU Taxonomy Regulation, and the EU Non-Financial Reporting Directive (NFRD).

The European Banking Authority (EBA) is responsible for overseeing the implementation of the Basel III reforms, which include principles for the effective management and supervision of climate-related financial risks, as well as the EU Bank Recovery and Resolution Directive (BRRD).

At the same time, global regulators are following the EU’s example and bringing in regulations to drive sustainability and enable a green transition. These initiatives include the China Securities Regulatory Commission’s Green Securities Guidelines, the Japan Financial Services Agency’s law that mandates banks to submit additional ESG information, and the Australian Prudential Regulation Authority’s Climate Vulnerability Assessment.

In addition, the US Federal Reserve Board launched a climate scenario analysis exercise to enable supervisors and firms to measure and manage climate-related financial risks where scenario analysis is a key component. Similarly, the Office of the Superintendent of Financial Institutions (Canada) published Guideline B-15 on climate risk management with climate scenario analysis a key tenet of the guideline. In the UK, the Bank of England and the Prudential Regulation Authority have mandated climate stress tests for banks as well as scenario analysis and risk appetite assessment.

UNDERSTANDING CLIMATE TRANSITION RISK

Transition risk refers to the financial risks that come with the shift to a low-carbon and sustainable economy.

It includes the potential negative impact on businesses and investments due to:

- Policy and regulatory changes, such as carbon pricing, emissions regulations, or renewable energy incentives, and the cost of compliance

- Technology shifts, including development and adoption of new technologies to mitigate climate change, and their potential to disrupt industries and render business models obsolete

- Market dynamics, including changing consumer preferences and investor demands for sustainable products and services

- Physical risks, including extreme weather events or resource scarcity that can directly impact businesses and investments

Climate transition risk measurement requires the application of a relevant data and analytics approach that captures and tracks the impact of all of the above on assets, including investments and loan portfolios. Such data must be standardized for comparison across asset classes, sectors and regions, as well as sufficiently robust to accommodate back- and forward-testing.

THE ROLE OF SCENARIO ANALYSIS IN ACHIEVING COMPLIANCE

Climate scenario analysis, a concept still at nascency, will require a high degree of collaboration among businesses, policy makers, and climate modelers.

Climate regulatory frameworks require the disclosure of self-reported bottom-up data, such as carbon footprint data including Scope 1, 2, and 3 emissions. Most guidelines and rule sets further require scenario analysis to understand and manage climate risks, especially transition risk. However, scenario modeling poses several challenges.

Climate scenario analysis and related stress testing, which is critical to financial institutions’ compliance, are still disciplines in the making. They require a high level of intra-disciplinary collaboration among climate modelers, economists and policy experts, as well as investment and risk professionals. Industry practices also suffer from a lack of consistent and objective data. The immaturity of the scenario modeling discipline was highlighted by the Bank of England in the results of the Climate Biennial Exploratory Scenario aimed at exploring the financial risks posed by climate change for banks and insurers.

OUR APPROACH TO ASSESSING TRANSITION RISK

Data will play a key role in calculating, and therefore mitigating, transition risk.

Banks and other financial institutions must consider the following factors while including climate stress tests in their risk management model:

Regulatory mandate: Given regulatory pressures and the urgency to develop climate scenario analysis frameworks that are transparent and help banks achieve compliance, banks must incorporate climate related stress tests into climate scenario modeling and determine the material and pecuniary impact on their loan book portfolios.

Data and analytics: Banks must develop transparent, sector- and region-specific scenarios, across asset classes, which can translate complex climate scenarios into fundamental financial performance drivers. This approach is rooted in the understanding that climate transition can play out in a wide variety of ways depending on many variables. To effectively manage risk, banks and financial institutions must assess more than one such pathway, or scenario, while also understanding the risks specific to a particular region or sector. Scenario analytics enable banks to carry out climate stress tests reflecting multiple climate and transition outcomes to generate empirical and quantitative ratings of assets and debts in their portfolios. This stress testing-based modeling will help banks to incorporate sustainability into their business strategies and risk management processes in compliance with country-specific regulatory requirements.

There are two main approaches to calculating transition risk:

- Top-down approach: This approach uses macroeconomic data to assess the impact of climate change on entire industries or sectors. It is relatively quick and easy to implement but can be less accurate than the bottom-up approach, as it does not consider the specific circumstances of individual organizations.

- Bottom-up approach: This approach analyzes the financial statements and other data of individual firms to assess their exposure to transition risk. While this approach is more accurate than the top-down approach, it is more time-consuming and expensive to implement.

Choosing the right transition risk methodology is critical. The best approach to calculating transition risk for a particular organization depends on a number of factors, including the size and complexity of the firm, the availability of data, and the resources available to conduct the analysis. Many risk managers rely heavily on self-reported or bottom-up data (for example, carbon emissions). But such data is subject to inaccuracy and inconsistency across firms, sectors, and regions. It also tells only part of the story, for example by considering only abatement costs but not revenue impacts. Though the choice of method depends on an institution’s specific needs, comparable, standardized data that tracks the impact of a broad range of climate and economic factors (top-down data) offers clear advantages. Financial institutions can get a more comprehensive understanding of their exposure to transition risk and make informed decisions about how to manage it by using a combination of the two methods.

HOW TCS CAN HELP

TCS has partnered with Entelligent to build a climate scenario modeling offering.

It emphasizes top-down inputs while also considering bottom-up data and can be executed at different degrees of granularity.

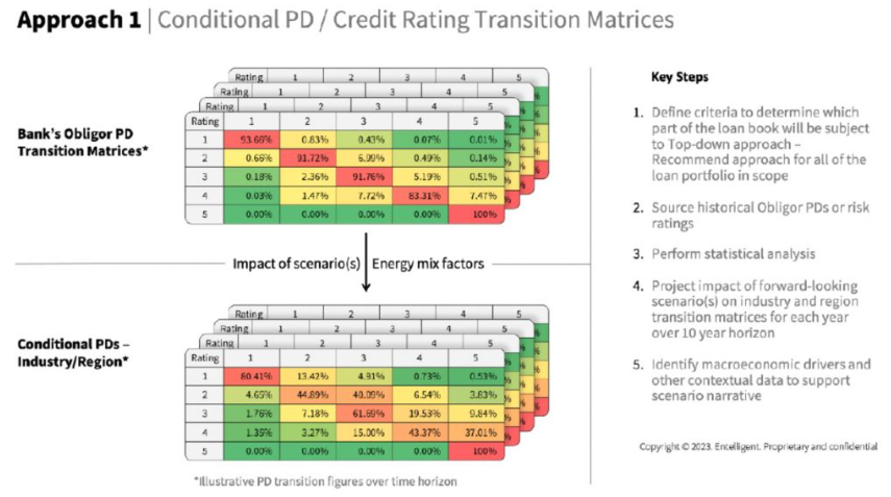

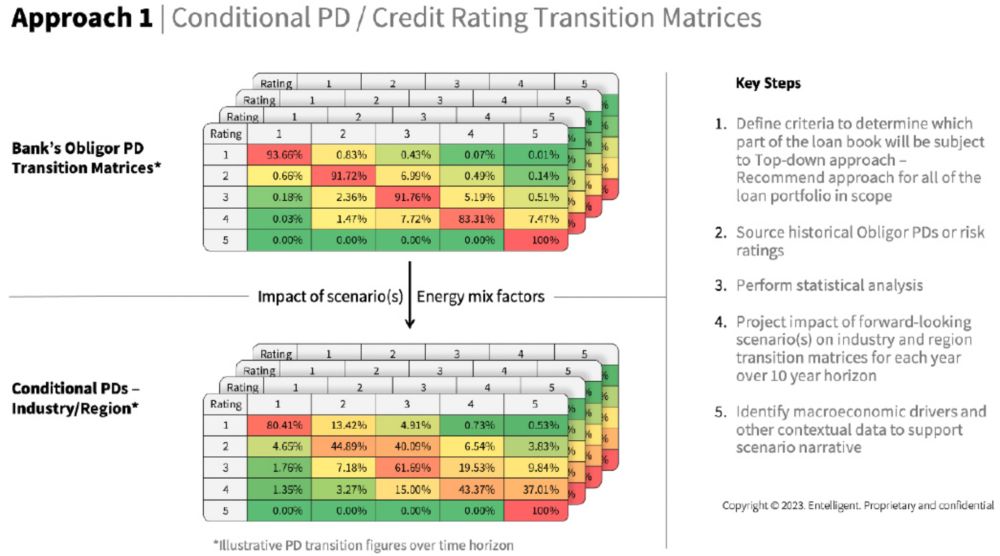

Less granular – credit rating or probability of default (PD) approach: Transition risk is modeled based on the sensitivities of the financial services industry and regional PDs to the transitioning entity’s energy factors (see Figure 1). This approach provides a comprehensive perspective on transition risk. It is generally faster to execute, covers a broad range of assets, and provides a firm-wide perspective on the transition’s implications.

Figure 1: Top-down approach to climate risk modeling

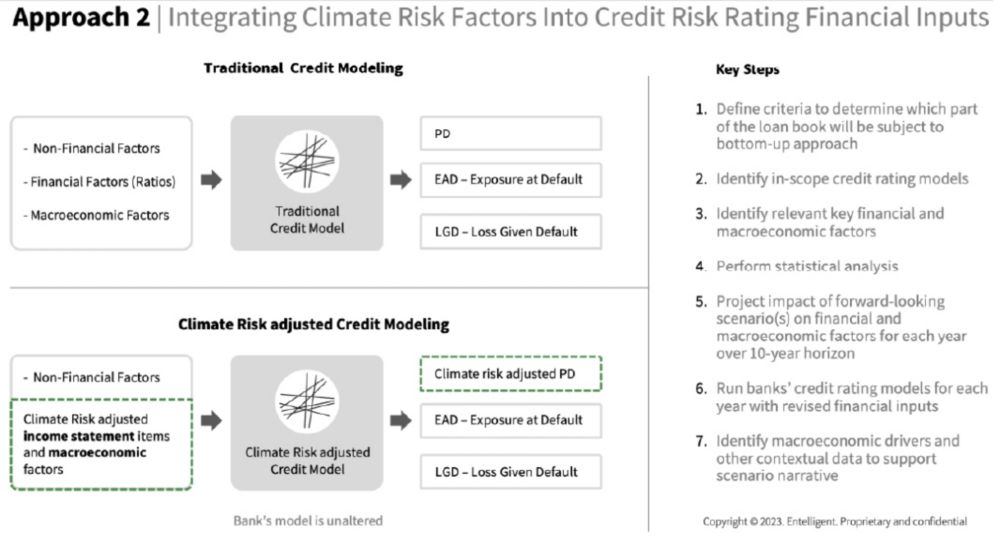

More granular – credit ratings and financial inputs approach: This approach relies on publicly available or company-provided financial statement data, modeling company-specific transition risk based on the sensitivities of key financial ratios’ to the transitioning entity’s energy factors (see Figure 2). This approach is best applied in more-targeted use cases, for example, where obligors are large, publicly traded entities.

Figure 2: Bottom-up approach to climate risk modeling

Factoring in climate risk is critical for banks to ensure sustainable operations and comply with regulations. While climate risk modeling is complex, solutions do exist. Banks and financial institutions that incorporate climate risk into their existing risk management frameworks are better positioned to lead the charge toward a greener economy.

*IMF, Equity Investors Must Pay More Attention to Climate Change Physical risk, May 2020

ABOUT THE AUTHORS

Pooja Khosla is a data scientist and econometrician with extensive experience in finance. She is an inventor of Entelligent’s patented Smart Climate® technology. She has a B.S. in Economics and Mathematics and an M.S. in Econometrics and Quantitative Economics from the University of Rajasthan, and an M.S. and Ph.D. in Economics from the University of Colorado, Boulder.

Fenton Aylmer, a banking risk management veteran, is the President of Donadea, Inc., a strategy and risk advisory services company. He is a lecturer in the Enterprise Risk Management Master of Science program at Columbia University’s School of Professional Studies. He also serves as Entelligent’s Banking Solutions Lead and is the creator of its Loan Book application.

Piyush Srivastava is a senior capital markets professional and risk management expert with TCS’ Banking, Financial Services, and Insurance (BFSI) business unit. Over the past several years, Piyush has helped many clients with transformation projects that transcend capital market business processes, risk, compliance, and digital transformation.